We solve all your doubts, so we are on the same page

We answer all your questions in straightforward language.

If you have a variable rate mortgage and your instalments have barely changed since 2008, it is more than likely that you have a ‘floor clause’. You can find out by checking the deed for your mortgage loan. It would appear under “limits to interest rate variance”.

You can send us your mortgage loan deed with our form. It will take you less than 99 seconds. We will analyse the unfair terms of your mortgage and file a claim for all of them. This way, we make sure you are getting the maximum amount you are entitled to.

The problem stems from the fact that many banks don’t provide clear information on the existence of this clause, or its implications. This practice is punishable by law. If a clause does not pass the transparency test, a judge would classify it as unfair, and therefore null and void. If this is the case, you can claim.

The aim is to obtain a favourable ruling to annul this ‘floor clause’ in your mortgage if you are still paying back the amounts owed. You can reclaim your money back even if you have already paid it off.

Yes. If the judge declares the ‘floor clause’ to be null and void, you can claim even if you have signed an agreement. The same rule applies if you have reached an out-of-court settlement and you are not satisfied with the offer received. Or if they have refused to reimburse your money. In such cases, you can always resort to the courts, to make a claim for everything you are entitled to.

A very high percentage of these types of claims are accepted. However, it is difficult to predict exactly how the procedure will end.

What we can say is that we are very confident in what we do, and in how we do it. That’s why we are committed to our no No Win No Fee policy. In addition, during the process, you can always include our legal expenses insurance. This way you’ll have nothing to worry about in the unlikely event that your claim is unsuccessful.

It depends on the judge’s decision in regard to the transparency test of the affected clause. If the judge considers that it does not pass said test, it will be declared unfair, and therefore null and void. This means that you would get your money back.

According to the Spanish Supreme Court, the clause cannot pass the transparency test if you do not have a qualified financial operator profile and:

Yes, in fact, you can combine both in your claim. This would increase the amount of money to be reimbursed.

You can send us your mortgage loan deed with our form. It will take you less than 99 seconds. We will analyse the unfair terms of your mortgage and file a claim for all of them. This way, we make sure you are getting the maximum amount you are entitled to.

All you have to do is fill out our form, with the information we ask from you. You will reach a point where we will ask you to attach the following documentation if you have it. If not, we will let you know how to obtain it during the process.

If you also want to reclaim your mortgage costs, we will also need:

In all mortgage claims, the principal document that must be provided is the deed of the mortgage loan. It is important not to confuse it with the title deed.

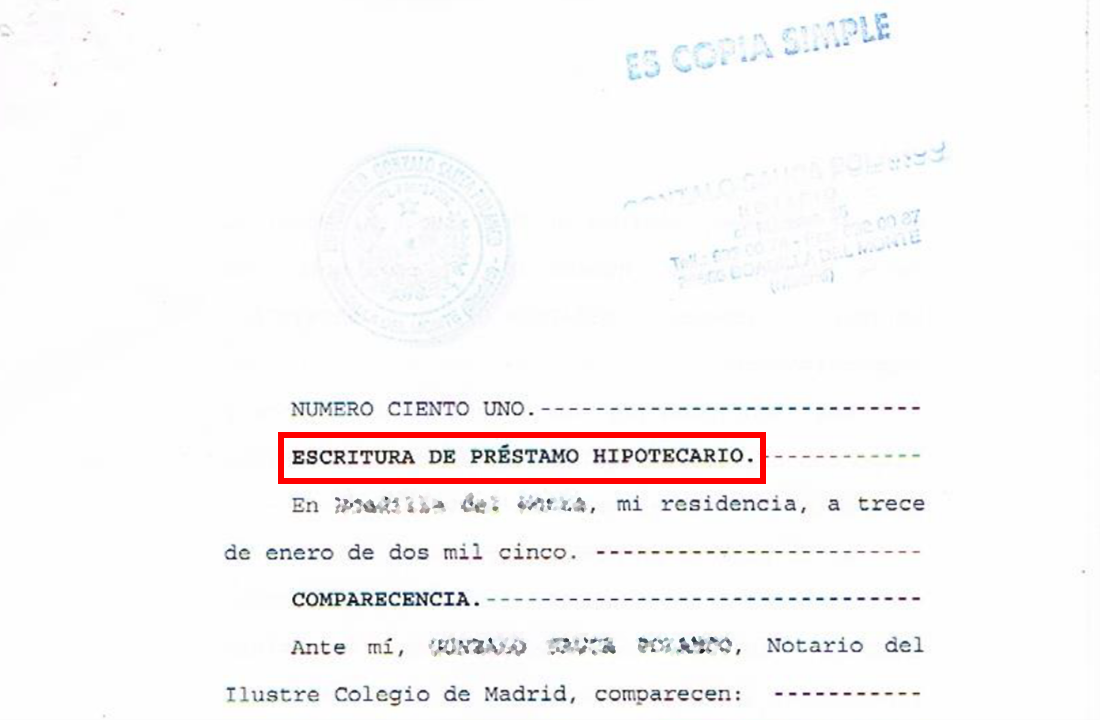

To identify the mortgage loan deed, we should look at the title of the document itself. This usually refers to “Escritura de préstamo hipotecario”.

Here is an example of a mortgage loan deed.

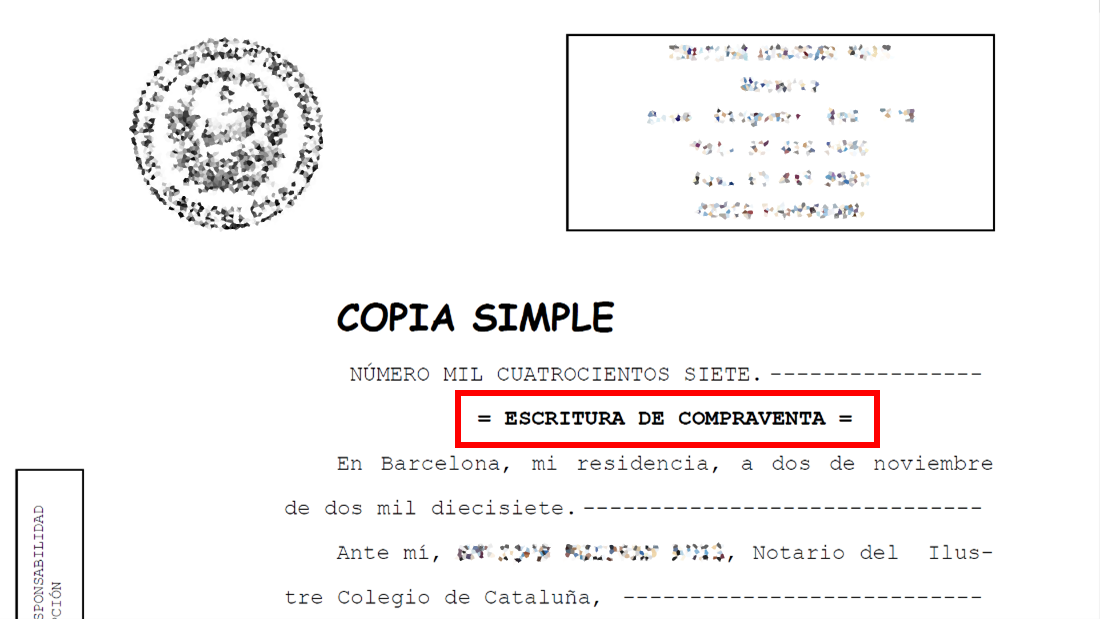

The title deed can be identified in the same way. The title refers to “Escritura de Compraventa”. Here is an example. And we like to stress the fact that this is not the document we need.

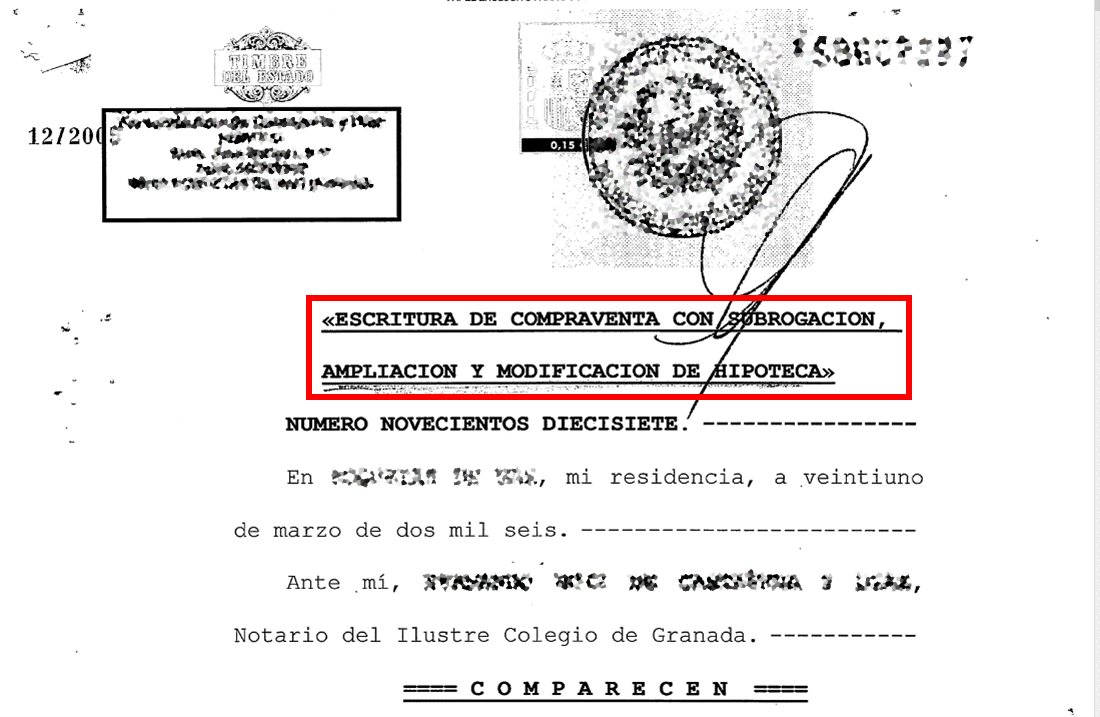

Note: there are deeds entitled as “Escritura de compraventa con garantía hipotecaria, subrogación, novación o ampliación”. These deeds, although they contain the word “compraventa” in the title, would also be valid to claim certain abusive mortgage clauses. Here is an example.

What if you get back more money than you expected?

It's normal to not be aware of everything you can claim. The same can be said regarding the protection of your interests. You can find out in under 99 seconds by answering a few simple questions.

I want to startIt's normal to not be aware of everything you can claim. The same can be said regarding the protection of your interests. You can find out in under 99 seconds by answering a few simple questions

{kind=link}

{kind=link}

{kind=link}