We solve all your doubts, so we are on the same page

We answer all your questions in straightforward language.

You don’t have to worry about a thing, from start to finish. There are several stages in the process. We’ll be in touch at least once a month or each time there are updates on your claim. You’ll always have access through your account.

The first step is to lodge an out-of-court complaint to try to reach an agreement. If this is not possible, we’ll proceed to make a claim. If the claim is admitted for processing by the judge, he/she will inform the respondent about the trial. In some cases, your presence may be required. If so, we’ll let you know in advance and give you all the necessary information. After this, the judge will issue a ruling. And if it’s favourable, the deadline to recover your money starts.

It’ll depend on the type of claim and the court’s caseload. Some claims will be resolved in months, others may take years.

No. You don’t have to pay a single euro in advance. We’ll upfront all costs, including the solicitor and power of attorney. You’ll only pay our fees if you win your claim.

It depends on how many requests each court is facing. In some the process takes longer, and others are faster.

There are two ways:

They’re costs incurred by each of the parties involved in legal proceedings. These are the fees of Lawyers, Court representatives, and expert witness fees (if necessary). As well as copies, court notices or registered faxes, among others. When the court allocates costs, it means the losing party has to pay these expenses for the opposing party.

That’s why we always give you the option to include our insurance. So you don’t have to worry if your claim is unsuccessful. We’ll cover all costs that may be incurred against you.

So you can file your claim free of charge, we take on a huge financial burden. What’s more, plaintiffs in mass claims try to delay compensation payments for as long as possible. While knowing that this means our chances of incurring heavy losses will increase.

That’s why, if the court allows it, we retain the interest and court costs imposed on the other party as fees, under article 44.2 of the Spanish General Statute of the Legal Profession. This ensures continuity in our project. And that everyone can access justice to defend their rights in an easy, convenient, and affordable way.

It is a power of attorney that you grant us so that we can represent you and carry out your claim. It has no cost and is 100% online. You can do it in two ways:

You decide. Whichever option you choose, we will explain you how to do it step by step during the claim process.

We’ll let you know the status of your claim at least once a month by email or text message. And you can access your account whenever you want. In real-time. All-year-round. You’re in control. We’re transparent from start to finish.

The Estimated Date of Termination of your claim is calculated based on an algorithm developed by in99.

Yes, it is completely normal and a sign that the algorithm is working correctly.

Like the navigation system in your smartphone or car that calculates an Estimated Time of Arrival (ETA) to your destination, our algorithm considers a multitude of factors to provide you with an Estimated Date of Termination of the claim. In a navigation system, the initial estimate considers factors such as the route, kilometers to destination, average speed on each road and even the density of the traffic if they are sophisticated enough. However, you may be halfway of the journey and it is normal to find that these factors are slightly different than originally estimated and therefore resulting in an updated Estimated Time of Arrival (your speed may be faster or slower than originally estimated, the traffic density higher or lower than estimated, etc …). The Estimated Time of Arrival changes as frequently as these factors change. Our algorithm that calculates the Estimated Date of Completion works in a similar way. As in a navigation system, the closer we get to the destination, the more precise and reliable the estimate becomes as the margin for these factors to change narrows down. In other words, the closer we are to the Estimated Date of Completion of your claim, the more precise and reliable the forecast will become.

Please note that in any case the date is a mere automated estimate that is calculated based on multipole factors, which may not develop as expected. Thus, we do not recommend that you make any plans fully relying on these estimates, and we disclaim any type of responsibility otherwise.

As frustrating as it is, changes to the estimated completion date are completely out of our control.

We have a shared interest, not only in winning your claim. The sooner the better. Our fee system is based on “no win, no pay” and we anticipate all the costs of your claim. This means that the longer the claim lasts, the more uneconomic it will be for us.

In this regard, you can be sure that we share your frustration if the completion date of your claim is delayed. The only thing we can do is continue to keep you informed at all times to the best of our knowledge.

All documents that you want to submit to your claim must meet the following requirements:

The documents you share with us will be the ones we will present to the court with your claim. That’s why they need to be clear and legible. In other words, they must be clearly readable.

You can get a clear photograph if you:

Here is an example of a legible document.

For heavier documents or documents with a larger number of pages, we recommend uploading the file in pdf format.

If you don’t have a scanner at hand, we show you other alternatives:

It may happen that the document you have uploaded is not exactly the one we need for the claim. You can check if the title of the document we request matches the document you have uploaded.

If you have a variable rate mortgage and your instalments have barely changed since 2008, it is more than likely that you have a ‘floor clause’. You can find out by checking the deed for your mortgage loan. It would appear under “limits to interest rate variance”.

You can send us your mortgage loan deed with our form. It will take you less than 99 seconds. We will analyse the unfair terms of your mortgage and file a claim for all of them. This way, we make sure you are getting the maximum amount you are entitled to.

The problem stems from the fact that many banks don’t provide clear information on the existence of this clause, or its implications. This practice is punishable by law. If a clause does not pass the transparency test, a judge would classify it as unfair, and therefore null and void. If this is the case, you can claim.

The aim is to obtain a favourable ruling to annul this ‘floor clause’ in your mortgage if you are still paying back the amounts owed. You can reclaim your money back even if you have already paid it off.

Yes. If the judge declares the ‘floor clause’ to be null and void, you can claim even if you have signed an agreement. The same rule applies if you have reached an out-of-court settlement and you are not satisfied with the offer received. Or if they have refused to reimburse your money. In such cases, you can always resort to the courts, to make a claim for everything you are entitled to.

A very high percentage of these types of claims are accepted. However, it is difficult to predict exactly how the procedure will end.

What we can say is that we are very confident in what we do, and in how we do it. That’s why we are committed to our no No Win No Fee policy. In addition, during the process, you can always include our legal expenses insurance. This way you’ll have nothing to worry about in the unlikely event that your claim is unsuccessful.

It depends on the judge’s decision in regard to the transparency test of the affected clause. If the judge considers that it does not pass said test, it will be declared unfair, and therefore null and void. This means that you would get your money back.

According to the Spanish Supreme Court, the clause cannot pass the transparency test if you do not have a qualified financial operator profile and:

Yes, in fact, you can combine both in your claim. This would increase the amount of money to be reimbursed.

You can send us your mortgage loan deed with our form. It will take you less than 99 seconds. We will analyse the unfair terms of your mortgage and file a claim for all of them. This way, we make sure you are getting the maximum amount you are entitled to.

All you have to do is fill out our form, with the information we ask from you. You will reach a point where we will ask you to attach the following documentation if you have it. If not, we will let you know how to obtain it during the process.

If you also want to reclaim your mortgage costs, we will also need:

In all mortgage claims, the principal document that must be provided is the deed of the mortgage loan. It is important not to confuse it with the title deed.

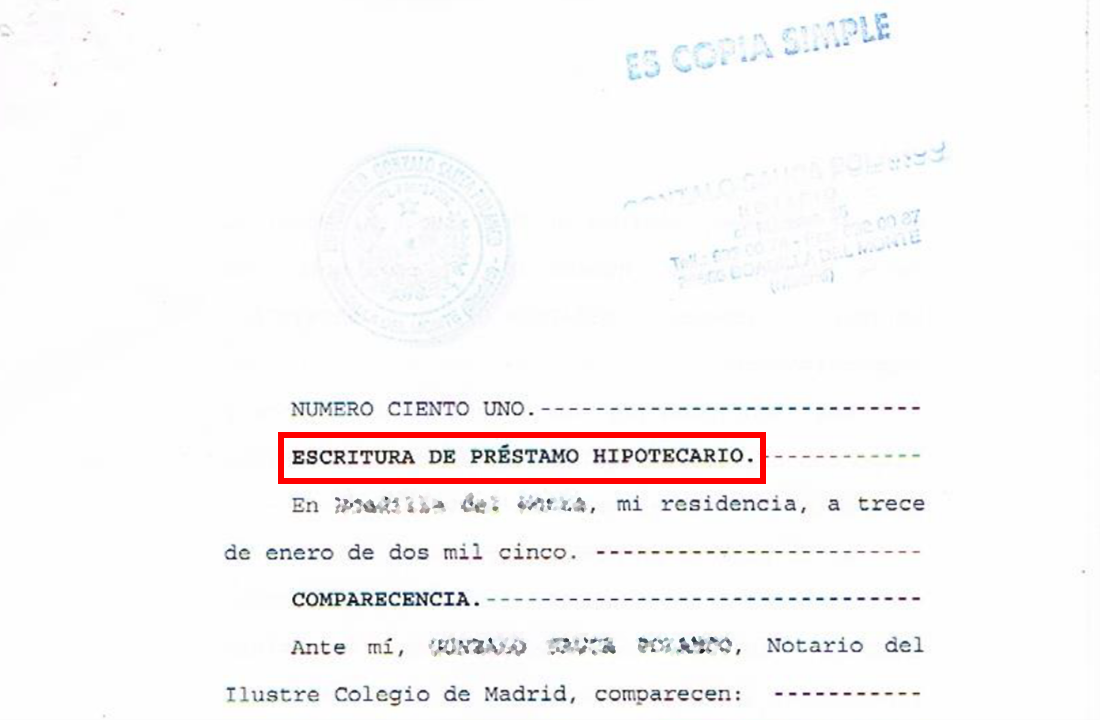

To identify the mortgage loan deed, we should look at the title of the document itself. This usually refers to “Escritura de préstamo hipotecario”.

Here is an example of a mortgage loan deed.

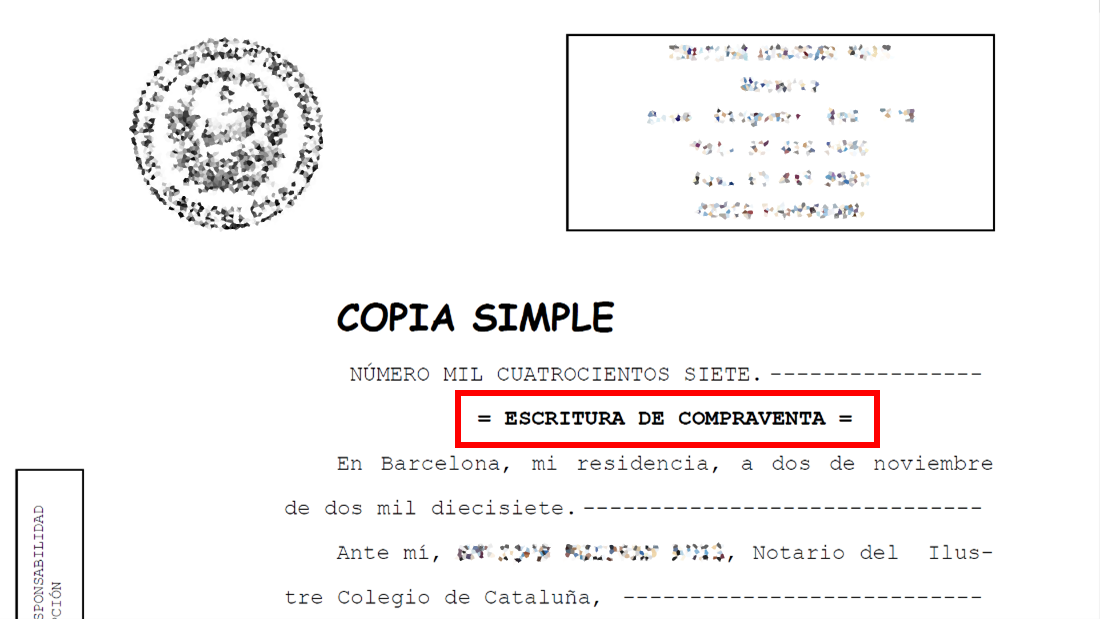

The title deed can be identified in the same way. The title refers to “Escritura de Compraventa”. Here is an example. And we like to stress the fact that this is not the document we need.

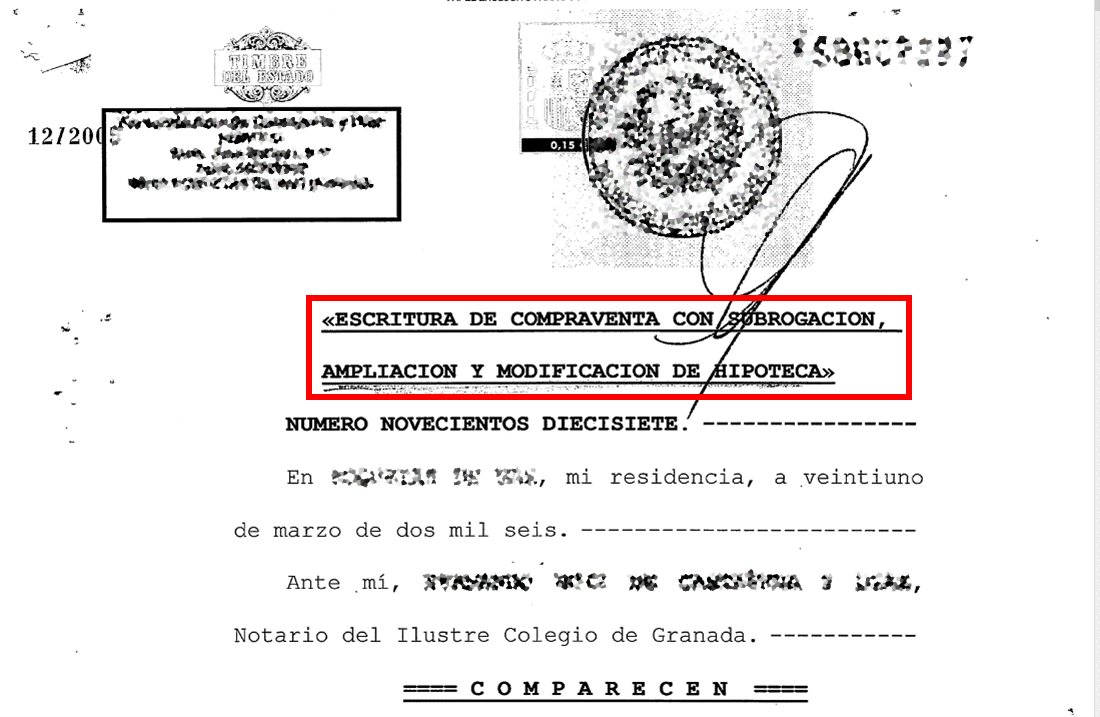

Note: there are deeds entitled as “Escritura de compraventa con garantía hipotecaria, subrogación, novación o ampliación”. These deeds, although they contain the word “compraventa” in the title, would also be valid to claim certain abusive mortgage clauses. Here is an example.

You can claim most of the costs of setting up your mortgage. These are the agency fees, notaryfees (only 50%), registration fees, appraisal fees and arrangement fee.

If you have or have ever had a mortgage loan, it is very likely that you have paid incorporation expenses and set up costs. This is because banks often include it as a clause within mortgage loans

You can start your claim by filling in our form. It will take you less than 99 seconds. We will analyse the unfair terms of your mortgage and file a claim for all of them. This way, we make sure you are getting the maximum amount you are entitled to.

The Spanish Supreme Court considers that the party who benefits the most from registering the mortgage deed is the bank. Therefore, it must bear most of these costs.

If your mortgage was signed before 10 November 2018, you cannot claim this tax. The Spanish Supreme Court ruled that in this case the buyer is liable for payment.

A very high percentage of these types of claims are accepted. However, it is difficult to predict exactly how the procedure will end.

What we can say is that we are very confident in what we do, and in how we do it. That’s why we are committed to our no No Win No Fee policy. In addition, during the process, you can always include our legal expenses insurance. This way you’ll have nothing to worry about in the unlikely event that your claim is unsuccessful.

The aim is to obtain a favourable ruling, declaring the clause which imposed these costs on you, null and void. You will be able to recover all or a part of these amounts

All you have to do is fill out our form with the information we ask from you. You will reach a point where we will ask you to attach this documentation if you have it. If not, we will let you know how you can obtain it during the process.

To claim mortgage costs you’ll need:

In all mortgage claims, the invoices that must be provided are those associated with the mortgage loan. It is important not to confuse these with the invoices associated with the title or sales deed.

To identify the invoices related to the mortgage loan deed, we must look at the title of the document. The title usually refers to “mortgage”, “mortgage loan”.

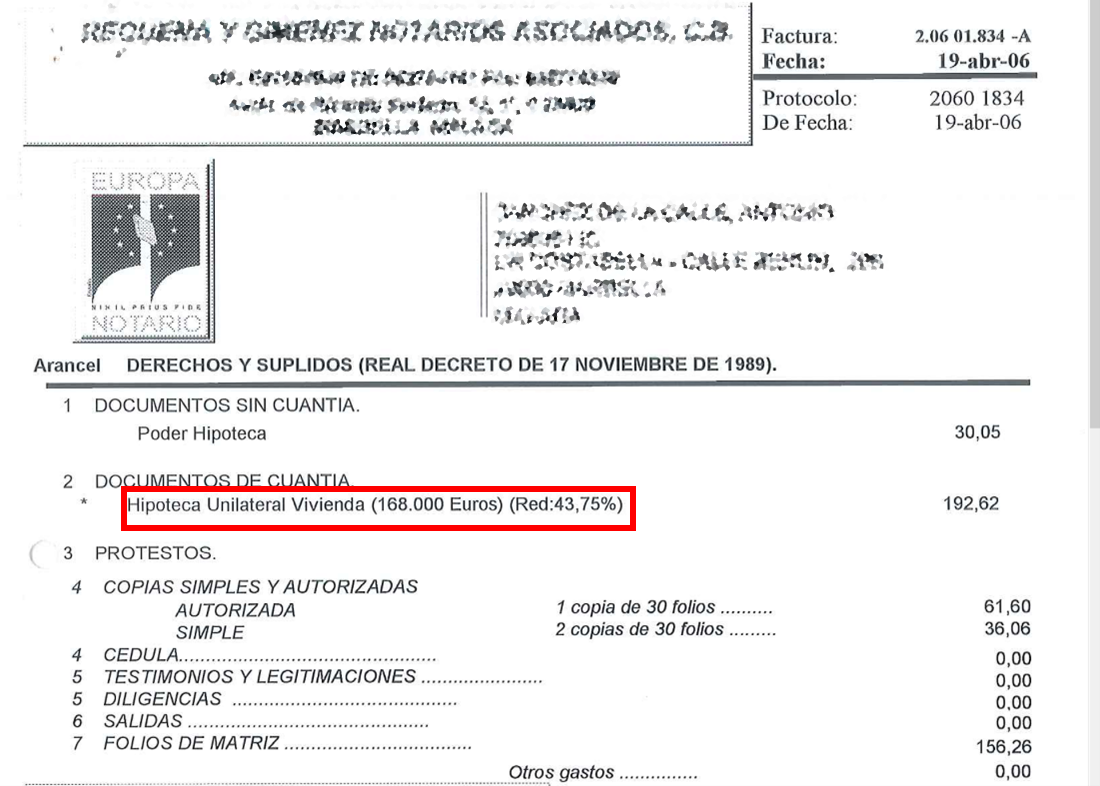

Here is an example of an invoice for notary fees.

Here is an example of a registration invoice.

Indeed, we have had many successful outcomes on revolving credit card claims. Every client is different. The end result and amount recovered will depend on your situation. However, we can confirm that these claims have a high success rate. These are just some of the cases we have won:

You can find out by considering the following:

You can start your claim by filling in our form. It will take you less than 99 seconds.

To find out whether a credit card is subject to excessive interest rates, we must analyse the card’s details. There are certain revolving credit cards that seem eligible to claim: WiZink, revolving Cetelem, revolving Citibank, Cofidis, and the Carrefour Pass. Even so, every card should be examined.

These are just examples. It’s likely that one of the cards you have in your wallet is affected. Regardless of the financial institution. If you have accepted a very low fixed monthly fee, you may be paying excessive interest with each day that passes.

Mainly because you were charged excessive interest rates. The Spanish Supreme Court determined that an interest rate is considered excessive if it is significantly higher than average market interest rates. And this is what occurs with revolving credit cards.

A very high percentage of these types of claims are accepted. However, it is difficult to predict exactly how the procedure will end.

What we can say is that we are very confident in what we do, and in how we do it. That’s why we are committed to our no No Win No Fee policy. In addition, during the process, you can always include our legal expenses insurance. This way you’ll have nothing to worry about in the unlikely event that your claim is unsuccessful.

The goal is to cancel your revolving credit card contract and get reimbursed for the money you have overpaid. Since the interest rate is so high, we could be talking about significant amounts.

Your claim’s outcome will always depend on the individual circumstances of your case. Perhaps you haven’t paid back everything you have borrowed. In this case, it’s possible that there isn’t anything to be reimbursed by the financial institution.

What do we do if this is the case? We apply for the interest rate to be declared null and void. Therefore, you would no longer have to pay interest. This means you will pay less on the outstanding debt or, in other words, pay only the amount initially taken out. Interest-free.

So, if you’re in a similar situation, it is in your best interest to make a claim. This way, even if you don’t get any money back, you could still pay less and settle your debt. What’s more, with in99 you don’t have to pay a single euro upfront. We only get paid if your case is won. And if you’re worried about losing your case, we offer a legal fee insurance policy to cover the trial costs, in the unlikely event that you don’t win. Without any risks.

All you have to do is fill out our form with the information we ask from you. You will reach a point where we will ask you to attach this documentation if you have it. If not, we will let you know how you can obtain it during the process.

To make a claim on a revolving credit card, you’ll need certain supporting documents.

You will need to provide the contract you signed with the financial institution. If you don’t have your contract, another option is the amortisation table. This will show all the movements on your revolving credit card. This information will allow us to calculate how much you have overpaid.

You also have the option to send us your statements/settlements and we will take care of looking for the rest of the information for you. You can generally find these bank statements on your online account.

What can you do if you don’t have the contract or the amortisation table? In this case, you should contact the financial institution that offered you the line of credit and ask for a copy of both documents (your contract and amortisation table).

This request can be done both at the branch or online via their website.

When you manage to get in touch with them to ask for a copy of the documents, they will know that you need them to make a claim and they are likely to offer you a settlement. Our advice is to not sign any agreement, no matter how good it may seem. You may find yourself unknowingly giving up your right to take legal action and what they offered you was simply a reduced interest rate. This will then make it impossible for you to defend your rights as a consumer.

No, they’re two separate things. If you have a credit card and you purchase something, you pay the financial entity the amount due the following month. And the debt is paid off.

If you have a revolving credit card, you pay back the borrowed amounts in several instalments

with high interest rates. As a result, your debt is dragged out over time.

This will depend on the card’s use. If you used it to make business-related payments, such as paying suppliers or self-employment taxes, we would have to take a closer look at your case.

It is a mortgage loan taken out with a bank in a foreign currency, usually in yen or Swiss francs, and is indexed by the Libor. If you have one, it is more than likely that you have paid more than you would if you had a mortgage in euros and indexed by the Euribor.

You can start your claim by filling in our form. It will take you less than 99 seconds.

The Spanish Supreme Court and the Court of Justice of the European Union have ruled on the matter. They declared that multi-currency mortgages must be converted into euros if they do not pass the transparency test. This occurs when the consequences of taking it out have not been clearly and plainly explained. And, if you aren’t a financial or currency exchange expert.

Your monthly mortgage repayments vary constantly. This is due to fluctuations in the currency in which you have taken out the loan.

Over the past few years, exchange rates have not been unfavourable. This has led to substantial increases in your monthly instalments, as well as in the total amount owed. What’s more, the more time that passes, the more it will increase.

Our recommendation is that you claim. You can start by filling in our form. It will take you less than 99 seconds.

The aim is to annul the section of the contract on foreign currency in order to:

A very high percentage of these types of claims are accepted. However, it is difficult to predict exactly how the procedure will end.

What we can say is that we are very confident in what we do, and in how we do it. That’s why we are committed to our no No Win No Fee policy. In addition, during the process, you can always include our legal expenses insurance. This way you’ll have nothing to worry about in the unlikely event that your claim is unsuccessful.

Our recommendation is to not sign anything. You should know that if you take the settlement, it is very likely that you’ll be giving up a large part of the claim.

All you have to do is fill out our form with the information we will ask from you. You will reach a point where we will ask you to attach this documentation if you have it. If not, we will let you know how you can obtain it during the process.

Between 2006 and 2013, major car manufacturers joined forces under the name El Club de las Marcas (‘The Brand Club’) with one main objective: to form a cartel. They controlled price fixing of the motor vehicles market for 7 years. As a result, millions of people overpaid for their car, much more than they would have if it weren’t for these abusive practices.

The brands concerned made up for 90% of the market share. These are Citroën, Mitsubishi, BMW, Chevrolet, Chrysler, Jeep, Dodge, Fiat, Alfa Romeo, Lancia, Ford, Opel, Honda, Hyundai, Kia, Mazda, Mercedes, Nissan, Peugeot, Porsche, Renault, Seat, Toyota, Lexus, Audi, Volkswagen, Škoda and Volvo.

If you bought, leased or rented one or more cars between 2006 and 2013, it is more than likely that you paid more than you should have. You can start your claim by filling in our form. It will take you less than 99 seconds.

Yes, even if you’ve sold your car you can claim to get back the money you overpaid.

Anyone who has acquired one or more cars either by purchasing, leasing or renting one of the cartel’s brands between 2006 and 2013. Regardless of whether it was from an individual, a self-employed operator or a company.

It depends. If all the vehicles belong to the same company, you will only have to file one claim. If you have purchased many cars from different companies, you’ll have to submit a claim for each company.

In theory, yes. It’s a slightly more complicated process than with new cars, which is why we’d have to review your case in more detail. You can start you claim by filling in our form. It will take you less than 99 seconds.

If you have a viable case you can get back around 10% to 15% of the car’s price.

A very high percentage of these types of claims are accepted. However, it is difficult to predict exactly how the procedure will end.

What we can say is that we are very confident in what we do, and in how we do it. That’s why we are committed to our no No Win No Fee policy. In addition, during the process, you can always include our legal expenses insurance. This way you’ll have nothing to worry about in the unlikely event that your claim is unsuccessful.

All you have to do is fill out our form with the information that we will ask from you. You willreach a stage where we will ask you to attach this documentation if you have it. If not, we will let you know how you can obtain it during the process.

If you are unemployed or on sick leave, you should get in touch with the insurer to inform them of your situation. You will also need to know the deadlines and what documentation you’ll need to submit your application. After this, they should cover your instalments and provide a monthly notice detailing the coverage.

If this is not the case, we can help you defend your rights and claim what you are legally entitled to. You can begin by filling in our form. It takes less than 99 seconds.

It is an insurance policy that will cover all or part of your monthly instalments on your loan if you lose your job, or if you are on leave due to illness or injury.

The main issue with this type of insurance is that it is often included without the customer’s prior consent. Also, they often contain a number of coverage exclusions, i.e. specific situations in which the insurer will not be liable for paying out. They can add it to your contract even when they know you are affected by one of these exclusions.

You can start your claim by filling in our form. It will take you less than 99 seconds.

Although it is mostly included in mortgages, you can find this type of insurance in all kinds of loans. This is why we advise you to review all of your loan applications for the purchase of property to be repaid in monthly instalments. Such as, for the purchase of a vehicle. Even your housing rental agreement may include PPI.

No. This will be determined on a case-by-case basis and should be taken into account when signing. Read carefully through any coverage exclusions, waiting periods, if there are deductibles, the term period, and the maximum amounts that are insured. Such information must be concisely and transparently stated in the contract.

No, this type of insurance does not cover parental leave. It only covers the instalments of an employee who is unable to perform his/her duties due to sickness or injury. This will be subject to a doctor’s note issued by the Spanish Social Security.

No. This insurance is limited to workers who are in one of the following situations:

If you are displeased with this policy and you haven’t taken it out knowingly and voluntarily, you can and should file a claim. You can start by filling in our form. It will take you less than 99 seconds.

As with any claim, it is difficult to predict how the procedure will pan out.

What we can say is that we are very confident in what we do. And in how we do it. That’s why we are committed to our No Win No Fee policy. What’s more, during the process you can include our legal expenses insurance. This way you won’t have to worry about a thing in the unlikely event that your claim is unsuccessful.

All you have to do is fill in our form with the information we will ask from you. You will reach a point where we will ask you to attach this documentation if you have it. If not, we will let you know how you can obtain it during the process.

There are two regulations in force to assess how much and how passengers will be compensated by airlines. This will depend on the territory from which the flight took off/landed:

The vast majority of flight claims are subject to EU regulations. Most claims for flight delays and cancellations are focused on low-cost airlines. And these are the destinations most frequented.

In each case, the first thing we must take into account is the duration. You’re entitled to compensation for up to €600 when:

Through the Montreal Convention, it’s more complicated to estimate compensation, since it doesn’t specify the amount for delays or cancellations. Therefore, it’s up to the judge to decide the amount of compensation for the incident. In this case, we recommend claiming for delays over 12 hours.

You can also find out by filling out our form. It will take you less than 99 seconds. We will let you know if you are eligible to file a claim and an estimated amount. Free of charge and with no obligation.

If you arrived on time at the boarding gate and your documentation was in order, you can and should claim. Even if you were boarded on a different plane. As long as you didn’t voluntarily avoid boarding the plane. And if you arrived at your destination with, at least, a 3-hour delay.

Eu regulations foresee compensation for flight delays, cancellation, and overbooking. This is calculated based on the kilometres between the flight origin and destination:

You can also find out by filling out our form. It will take you less than 99 seconds. We will let you know if you are eligible to file a claim and an estimated amount. Free of charge and with no obligation.

Apart from compensation, you have other rights, depending on the case.

Delays:

Cancellation and overbooking:

Whatever your case may be, you can also claim:

Even if you no longer have your boarding pass, you can ask your airline for a boarding certificate. For this, you’ll need to make a written request to your airline. It’s important that you include the following information:

On average, it takes one year. This will depend on many factors, such as if the airline is willing to reach an out-of-court settlement or not.

These are extraordinary circumstances for which a flight may be delayed or cancelled. These are the only cases where it’s not possible to file a claim.

According to European regulations you have up to 5 years to make your claim from the date of the incident, regardless of whether it’s due to a delay, cancellation, or overbooking.

Through the Montreal Convention, you only have 2 years.

Your ID card or passport and your flight tickets or boarding pass are enough to justify and claim your flights.

To speed up the claim process, it’s advised to have one of the following documents at hand:

Generally, if you are in Spain for less than 183 days per year, you are not considered a resident for tax purposes. However, there are exceptions. For instance, if your spouse and children live in Spain, or if the Spanish tax office believes that your core economic interests are in Spain. You can also verify it by answering a few simple questions through our form. In less than 99 seconds.

That’s right. Even if you aren’t renting out your property, you’ll still have to pay what is known as allocated property income. By owning an empty or unused property, other than your ‘primary residence’, and deciding to not rent it out, the Spanish tax authorities consider that you could rent it out and generate income. Therefore they quantify this option for a certain amount and require you to pay tax on it.

If your property has been empty or used by you, a friend, or a relative for free, this would lead to an income allocation and you’ll have to pay tax.

Yes. The Spanish tax office makes no distinction on this matter. You have to pay taxes for allocated income.

If the taxpayer is a citizen of a European Economic Area (EEA) country the rate is 19%. If not, it will be 24%. This rate is applied on the taxable base and will vary depending on whether you are declaring income obtained from renting out the property or for the income allocation.

Yes, each owner must file their own tax return. Even if they are married.

You’ll have to file a tax return for each property you own in Spain.

Yes, you’re required to pay tax for allocated property income. This would amount to the number of days the property was in your name without being rented out, up until the date it was sold. Regardless of any other taxes that you’ll have to submit, such as those related to the sale itself.

If you don’t pay your taxes you would be breaking the law. Even if you live in a different country. It is likely the Spanish Tax Office will begin a verification process and you’ll face surcharges and penalties. These will accumulate until you settle your tax situation.

You’ll need your DNI or NIE handy. If you filed a tax return in Spain last year, we will also ask you for it. If not, we will ask you for the last five digits of your Spanish bank account’s IBAN.

You don’t have to worry about a thing, from start to finish. There are several stages in the process. We’ll be in touch at least once a month or each time there are updates on your claim. You’ll always have access through your account.

The first step is to lodge an out-of-court complaint to try to reach an agreement. If this is not possible, we’ll proceed to make a claim. If the claim is admitted for processing by the judge, he/she will inform the respondent about the trial. In some cases, your presence may be required. If so, we’ll let you know in advance and give you all the necessary information. After this, the judge will issue a ruling. And if it’s favourable, the deadline to recover your money starts.

It’ll depend on the type of claim and the court’s caseload. Some claims will be resolved in months, others may take years.

No. You don’t have to pay a single euro in advance. We’ll upfront all costs, including the solicitor and power of attorney. You’ll only pay our fees if you win your claim.

It depends on how many requests each court is facing. In some the process takes longer, and others are faster.

There are two ways:

They’re costs incurred by each of the parties involved in legal proceedings. These are the fees of Lawyers, Court representatives, and expert witness fees (if necessary). As well as copies, court notices or registered faxes, among others. When the court allocates costs, it means the losing party has to pay these expenses for the opposing party.

That’s why we always give you the option to include our insurance. So you don’t have to worry if your claim is unsuccessful. We’ll cover all costs that may be incurred against you.

So you can file your claim free of charge, we take on a huge financial burden. What’s more, plaintiffs in mass claims try to delay compensation payments for as long as possible. While knowing that this means our chances of incurring heavy losses will increase.

That’s why, if the court allows it, we retain the interest and court costs imposed on the other party as fees, under article 44.2 of the Spanish General Statute of the Legal Profession. This ensures continuity in our project. And that everyone can access justice to defend their rights in an easy, convenient, and affordable way.

It is a power of attorney that you grant us so that we can represent you and carry out your claim. It has no cost and is 100% online. You can do it in two ways:

You decide. Whichever option you choose, we will explain you how to do it step by step during the claim process.

We’ll let you know the status of your claim at least once a month by email or text message. And you can access your account whenever you want. In real-time. All-year-round. You’re in control. We’re transparent from start to finish.

The Estimated Date of Termination of your claim is calculated based on an algorithm developed by in99.

Yes, it is completely normal and a sign that the algorithm is working correctly.

Like the navigation system in your smartphone or car that calculates an Estimated Time of Arrival (ETA) to your destination, our algorithm considers a multitude of factors to provide you with an Estimated Date of Termination of the claim. In a navigation system, the initial estimate considers factors such as the route, kilometers to destination, average speed on each road and even the density of the traffic if they are sophisticated enough. However, you may be halfway of the journey and it is normal to find that these factors are slightly different than originally estimated and therefore resulting in an updated Estimated Time of Arrival (your speed may be faster or slower than originally estimated, the traffic density higher or lower than estimated, etc …). The Estimated Time of Arrival changes as frequently as these factors change. Our algorithm that calculates the Estimated Date of Completion works in a similar way. As in a navigation system, the closer we get to the destination, the more precise and reliable the estimate becomes as the margin for these factors to change narrows down. In other words, the closer we are to the Estimated Date of Completion of your claim, the more precise and reliable the forecast will become.

Please note that in any case the date is a mere automated estimate that is calculated based on multipole factors, which may not develop as expected. Thus, we do not recommend that you make any plans fully relying on these estimates, and we disclaim any type of responsibility otherwise.

As frustrating as it is, changes to the estimated completion date are completely out of our control.

We have a shared interest, not only in winning your claim. The sooner the better. Our fee system is based on “no win, no pay” and we anticipate all the costs of your claim. This means that the longer the claim lasts, the more uneconomic it will be for us.

In this regard, you can be sure that we share your frustration if the completion date of your claim is delayed. The only thing we can do is continue to keep you informed at all times to the best of our knowledge.

All documents that you want to submit to your claim must meet the following requirements:

The documents you share with us will be the ones we will present to the court with your claim. That’s why they need to be clear and legible. In other words, they must be clearly readable.

You can get a clear photograph if you:

Here is an example of a legible document.

For heavier documents or documents with a larger number of pages, we recommend uploading the file in pdf format.

If you don’t have a scanner at hand, we show you other alternatives:

It may happen that the document you have uploaded is not exactly the one we need for the claim. You can check if the title of the document we request matches the document you have uploaded.

If you have a variable rate mortgage and your instalments have barely changed since 2008, it is more than likely that you have a ‘floor clause’. You can find out by checking the deed for your mortgage loan. It would appear under “limits to interest rate variance”.

You can send us your mortgage loan deed with our form. It will take you less than 99 seconds. We will analyse the unfair terms of your mortgage and file a claim for all of them. This way, we make sure you are getting the maximum amount you are entitled to.

The problem stems from the fact that many banks don’t provide clear information on the existence of this clause, or its implications. This practice is punishable by law. If a clause does not pass the transparency test, a judge would classify it as unfair, and therefore null and void. If this is the case, you can claim.

The aim is to obtain a favourable ruling to annul this ‘floor clause’ in your mortgage if you are still paying back the amounts owed. You can reclaim your money back even if you have already paid it off.

Yes. If the judge declares the ‘floor clause’ to be null and void, you can claim even if you have signed an agreement. The same rule applies if you have reached an out-of-court settlement and you are not satisfied with the offer received. Or if they have refused to reimburse your money. In such cases, you can always resort to the courts, to make a claim for everything you are entitled to.

A very high percentage of these types of claims are accepted. However, it is difficult to predict exactly how the procedure will end.

What we can say is that we are very confident in what we do, and in how we do it. That’s why we are committed to our no No Win No Fee policy. In addition, during the process, you can always include our legal expenses insurance. This way you’ll have nothing to worry about in the unlikely event that your claim is unsuccessful.

It depends on the judge’s decision in regard to the transparency test of the affected clause. If the judge considers that it does not pass said test, it will be declared unfair, and therefore null and void. This means that you would get your money back.

According to the Spanish Supreme Court, the clause cannot pass the transparency test if you do not have a qualified financial operator profile and:

Yes, in fact, you can combine both in your claim. This would increase the amount of money to be reimbursed.

You can send us your mortgage loan deed with our form. It will take you less than 99 seconds. We will analyse the unfair terms of your mortgage and file a claim for all of them. This way, we make sure you are getting the maximum amount you are entitled to.

All you have to do is fill out our form, with the information we ask from you. You will reach a point where we will ask you to attach the following documentation if you have it. If not, we will let you know how to obtain it during the process.

If you also want to reclaim your mortgage costs, we will also need:

In all mortgage claims, the principal document that must be provided is the deed of the mortgage loan. It is important not to confuse it with the title deed.

To identify the mortgage loan deed, we should look at the title of the document itself. This usually refers to “Escritura de préstamo hipotecario”.

Here is an example of a mortgage loan deed.

The title deed can be identified in the same way. The title refers to “Escritura de Compraventa”. Here is an example. And we like to stress the fact that this is not the document we need.

Note: there are deeds entitled as “Escritura de compraventa con garantía hipotecaria, subrogación, novación o ampliación”. These deeds, although they contain the word “compraventa” in the title, would also be valid to claim certain abusive mortgage clauses. Here is an example.

You can claim most of the costs of setting up your mortgage. These are the agency fees, notaryfees (only 50%), registration fees, appraisal fees and arrangement fee.

If you have or have ever had a mortgage loan, it is very likely that you have paid incorporation expenses and set up costs. This is because banks often include it as a clause within mortgage loans

You can start your claim by filling in our form. It will take you less than 99 seconds. We will analyse the unfair terms of your mortgage and file a claim for all of them. This way, we make sure you are getting the maximum amount you are entitled to.

The Spanish Supreme Court considers that the party who benefits the most from registering the mortgage deed is the bank. Therefore, it must bear most of these costs.

If your mortgage was signed before 10 November 2018, you cannot claim this tax. The Spanish Supreme Court ruled that in this case the buyer is liable for payment.

A very high percentage of these types of claims are accepted. However, it is difficult to predict exactly how the procedure will end.

What we can say is that we are very confident in what we do, and in how we do it. That’s why we are committed to our no No Win No Fee policy. In addition, during the process, you can always include our legal expenses insurance. This way you’ll have nothing to worry about in the unlikely event that your claim is unsuccessful.

The aim is to obtain a favourable ruling, declaring the clause which imposed these costs on you, null and void. You will be able to recover all or a part of these amounts

All you have to do is fill out our form with the information we ask from you. You will reach a point where we will ask you to attach this documentation if you have it. If not, we will let you know how you can obtain it during the process.

To claim mortgage costs you’ll need:

In all mortgage claims, the invoices that must be provided are those associated with the mortgage loan. It is important not to confuse these with the invoices associated with the title or sales deed.

To identify the invoices related to the mortgage loan deed, we must look at the title of the document. The title usually refers to “mortgage”, “mortgage loan”.

Here is an example of an invoice for notary fees.

Here is an example of a registration invoice.

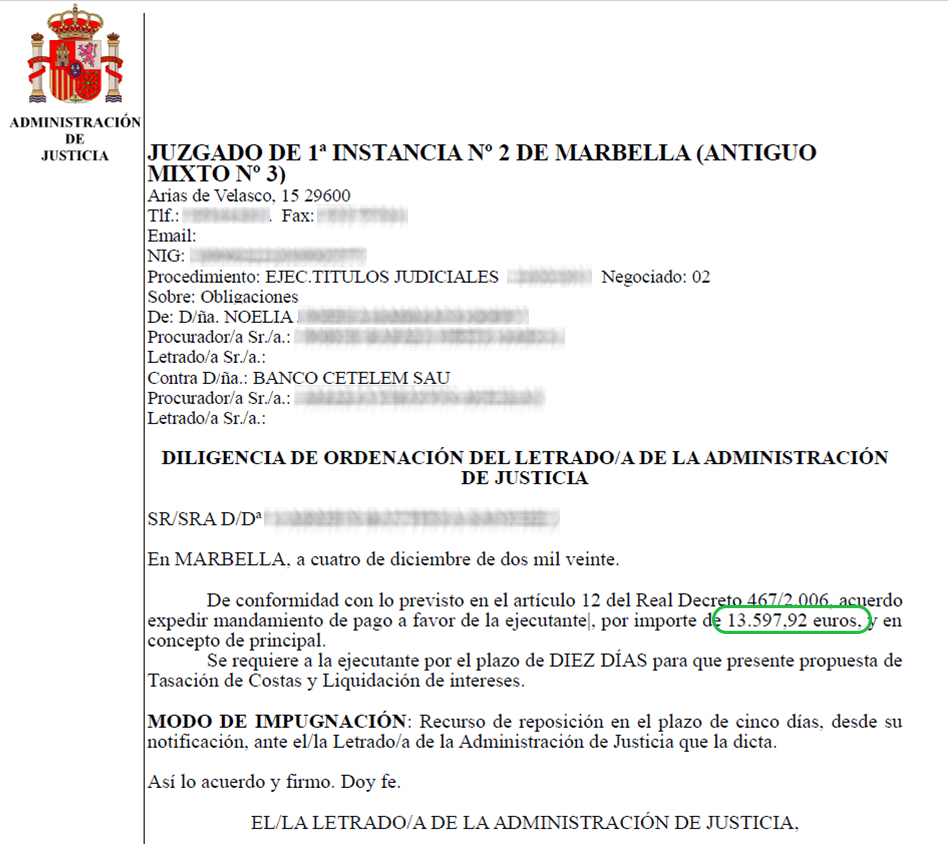

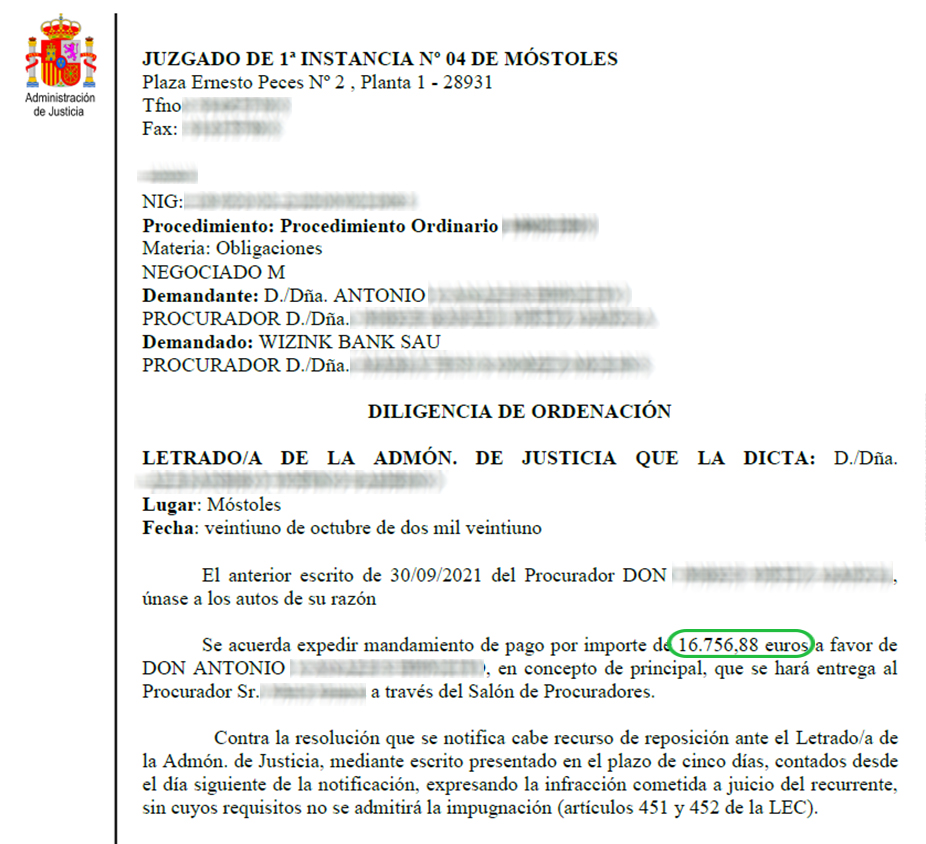

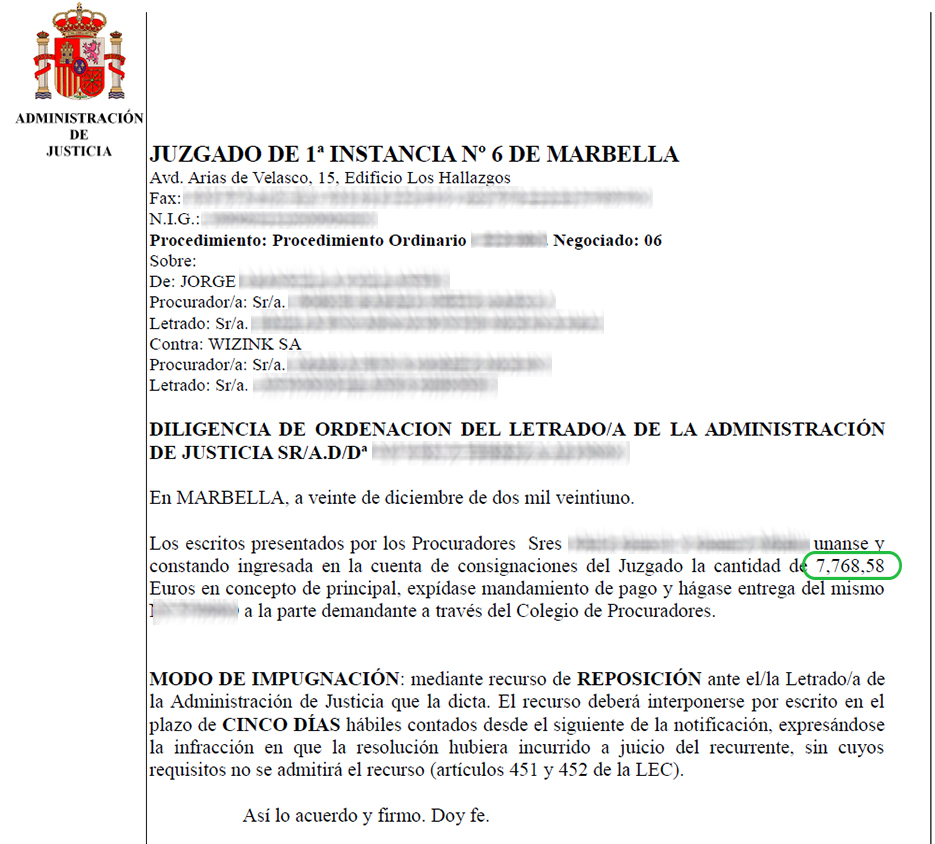

Indeed, we have had many successful outcomes on revolving credit card claims. Every client is different. The end result and amount recovered will depend on your situation. However, we can confirm that these claims have a high success rate. These are just some of the cases we have won:

You can find out by considering the following:

You can start your claim by filling in our form. It will take you less than 99 seconds.

To find out whether a credit card is subject to excessive interest rates, we must analyse the card’s details. There are certain revolving credit cards that seem eligible to claim: WiZink, revolving Cetelem, revolving Citibank, Cofidis, and the Carrefour Pass. Even so, every card should be examined.

These are just examples. It’s likely that one of the cards you have in your wallet is affected. Regardless of the financial institution. If you have accepted a very low fixed monthly fee, you may be paying excessive interest with each day that passes.

Mainly because you were charged excessive interest rates. The Spanish Supreme Court determined that an interest rate is considered excessive if it is significantly higher than average market interest rates. And this is what occurs with revolving credit cards.

A very high percentage of these types of claims are accepted. However, it is difficult to predict exactly how the procedure will end.

What we can say is that we are very confident in what we do, and in how we do it. That’s why we are committed to our no No Win No Fee policy. In addition, during the process, you can always include our legal expenses insurance. This way you’ll have nothing to worry about in the unlikely event that your claim is unsuccessful.

The goal is to cancel your revolving credit card contract and get reimbursed for the money you have overpaid. Since the interest rate is so high, we could be talking about significant amounts.

Your claim’s outcome will always depend on the individual circumstances of your case. Perhaps you haven’t paid back everything you have borrowed. In this case, it’s possible that there isn’t anything to be reimbursed by the financial institution.

What do we do if this is the case? We apply for the interest rate to be declared null and void. Therefore, you would no longer have to pay interest. This means you will pay less on the outstanding debt or, in other words, pay only the amount initially taken out. Interest-free.

So, if you’re in a similar situation, it is in your best interest to make a claim. This way, even if you don’t get any money back, you could still pay less and settle your debt. What’s more, with in99 you don’t have to pay a single euro upfront. We only get paid if your case is won. And if you’re worried about losing your case, we offer a legal fee insurance policy to cover the trial costs, in the unlikely event that you don’t win. Without any risks.

All you have to do is fill out our form with the information we ask from you. You will reach a point where we will ask you to attach this documentation if you have it. If not, we will let you know how you can obtain it during the process.

To make a claim on a revolving credit card, you’ll need certain supporting documents.

You will need to provide the contract you signed with the financial institution. If you don’t have your contract, another option is the amortisation table. This will show all the movements on your revolving credit card. This information will allow us to calculate how much you have overpaid.

You also have the option to send us your statements/settlements and we will take care of looking for the rest of the information for you. You can generally find these bank statements on your online account.

What can you do if you don’t have the contract or the amortisation table? In this case, you should contact the financial institution that offered you the line of credit and ask for a copy of both documents (your contract and amortisation table).

This request can be done both at the branch or online via their website.

When you manage to get in touch with them to ask for a copy of the documents, they will know that you need them to make a claim and they are likely to offer you a settlement. Our advice is to not sign any agreement, no matter how good it may seem. You may find yourself unknowingly giving up your right to take legal action and what they offered you was simply a reduced interest rate. This will then make it impossible for you to defend your rights as a consumer.

No, they’re two separate things. If you have a credit card and you purchase something, you pay the financial entity the amount due the following month. And the debt is paid off.

If you have a revolving credit card, you pay back the borrowed amounts in several instalments

with high interest rates. As a result, your debt is dragged out over time.

This will depend on the card’s use. If you used it to make business-related payments, such as paying suppliers or self-employment taxes, we would have to take a closer look at your case.

It is a mortgage loan taken out with a bank in a foreign currency, usually in yen or Swiss francs, and is indexed by the Libor. If you have one, it is more than likely that you have paid more than you would if you had a mortgage in euros and indexed by the Euribor.

You can start your claim by filling in our form. It will take you less than 99 seconds.

The Spanish Supreme Court and the Court of Justice of the European Union have ruled on the matter. They declared that multi-currency mortgages must be converted into euros if they do not pass the transparency test. This occurs when the consequences of taking it out have not been clearly and plainly explained. And, if you aren’t a financial or currency exchange expert.

Your monthly mortgage repayments vary constantly. This is due to fluctuations in the currency in which you have taken out the loan.

Over the past few years, exchange rates have not been unfavourable. This has led to substantial increases in your monthly instalments, as well as in the total amount owed. What’s more, the more time that passes, the more it will increase.

Our recommendation is that you claim. You can start by filling in our form. It will take you less than 99 seconds.

The aim is to annul the section of the contract on foreign currency in order to:

A very high percentage of these types of claims are accepted. However, it is difficult to predict exactly how the procedure will end.

What we can say is that we are very confident in what we do, and in how we do it. That’s why we are committed to our no No Win No Fee policy. In addition, during the process, you can always include our legal expenses insurance. This way you’ll have nothing to worry about in the unlikely event that your claim is unsuccessful.

Our recommendation is to not sign anything. You should know that if you take the settlement, it is very likely that you’ll be giving up a large part of the claim.

All you have to do is fill out our form with the information we will ask from you. You will reach a point where we will ask you to attach this documentation if you have it. If not, we will let you know how you can obtain it during the process.

Between 2006 and 2013, major car manufacturers joined forces under the name El Club de las Marcas (‘The Brand Club’) with one main objective: to form a cartel. They controlled price fixing of the motor vehicles market for 7 years. As a result, millions of people overpaid for their car, much more than they would have if it weren’t for these abusive practices.

The brands concerned made up for 90% of the market share. These are Citroën, Mitsubishi, BMW, Chevrolet, Chrysler, Jeep, Dodge, Fiat, Alfa Romeo, Lancia, Ford, Opel, Honda, Hyundai, Kia, Mazda, Mercedes, Nissan, Peugeot, Porsche, Renault, Seat, Toyota, Lexus, Audi, Volkswagen, Škoda and Volvo.

If you bought, leased or rented one or more cars between 2006 and 2013, it is more than likely that you paid more than you should have. You can start your claim by filling in our form. It will take you less than 99 seconds.

Yes, even if you’ve sold your car you can claim to get back the money you overpaid.

Anyone who has acquired one or more cars either by purchasing, leasing or renting one of the cartel’s brands between 2006 and 2013. Regardless of whether it was from an individual, a self-employed operator or a company.

It depends. If all the vehicles belong to the same company, you will only have to file one claim. If you have purchased many cars from different companies, you’ll have to submit a claim for each company.

In theory, yes. It’s a slightly more complicated process than with new cars, which is why we’d have to review your case in more detail. You can start you claim by filling in our form. It will take you less than 99 seconds.

If you have a viable case you can get back around 10% to 15% of the car’s price.

A very high percentage of these types of claims are accepted. However, it is difficult to predict exactly how the procedure will end.

What we can say is that we are very confident in what we do, and in how we do it. That’s why we are committed to our no No Win No Fee policy. In addition, during the process, you can always include our legal expenses insurance. This way you’ll have nothing to worry about in the unlikely event that your claim is unsuccessful.

All you have to do is fill out our form with the information that we will ask from you. You willreach a stage where we will ask you to attach this documentation if you have it. If not, we will let you know how you can obtain it during the process.

If you are unemployed or on sick leave, you should get in touch with the insurer to inform them of your situation. You will also need to know the deadlines and what documentation you’ll need to submit your application. After this, they should cover your instalments and provide a monthly notice detailing the coverage.

If this is not the case, we can help you defend your rights and claim what you are legally entitled to. You can begin by filling in our form. It takes less than 99 seconds.

It is an insurance policy that will cover all or part of your monthly instalments on your loan if you lose your job, or if you are on leave due to illness or injury.

The main issue with this type of insurance is that it is often included without the customer’s prior consent. Also, they often contain a number of coverage exclusions, i.e. specific situations in which the insurer will not be liable for paying out. They can add it to your contract even when they know you are affected by one of these exclusions.

You can start your claim by filling in our form. It will take you less than 99 seconds.

Although it is mostly included in mortgages, you can find this type of insurance in all kinds of loans. This is why we advise you to review all of your loan applications for the purchase of property to be repaid in monthly instalments. Such as, for the purchase of a vehicle. Even your housing rental agreement may include PPI.

No. This will be determined on a case-by-case basis and should be taken into account when signing. Read carefully through any coverage exclusions, waiting periods, if there are deductibles, the term period, and the maximum amounts that are insured. Such information must be concisely and transparently stated in the contract.

No, this type of insurance does not cover parental leave. It only covers the instalments of an employee who is unable to perform his/her duties due to sickness or injury. This will be subject to a doctor’s note issued by the Spanish Social Security.

No. This insurance is limited to workers who are in one of the following situations:

If you are displeased with this policy and you haven’t taken it out knowingly and voluntarily, you can and should file a claim. You can start by filling in our form. It will take you less than 99 seconds.

As with any claim, it is difficult to predict how the procedure will pan out.

What we can say is that we are very confident in what we do. And in how we do it. That’s why we are committed to our No Win No Fee policy. What’s more, during the process you can include our legal expenses insurance. This way you won’t have to worry about a thing in the unlikely event that your claim is unsuccessful.

All you have to do is fill in our form with the information we will ask from you. You will reach a point where we will ask you to attach this documentation if you have it. If not, we will let you know how you can obtain it during the process.

There are two regulations in force to assess how much and how passengers will be compensated by airlines. This will depend on the territory from which the flight took off/landed:

The vast majority of flight claims are subject to EU regulations. Most claims for flight delays and cancellations are focused on low-cost airlines. And these are the destinations most frequented.

In each case, the first thing we must take into account is the duration. You’re entitled to compensation for up to €600 when:

Through the Montreal Convention, it’s more complicated to estimate compensation, since it doesn’t specify the amount for delays or cancellations. Therefore, it’s up to the judge to decide the amount of compensation for the incident. In this case, we recommend claiming for delays over 12 hours.

You can also find out by filling out our form. It will take you less than 99 seconds. We will let you know if you are eligible to file a claim and an estimated amount. Free of charge and with no obligation.

If you arrived on time at the boarding gate and your documentation was in order, you can and should claim. Even if you were boarded on a different plane. As long as you didn’t voluntarily avoid boarding the plane. And if you arrived at your destination with, at least, a 3-hour delay.

Eu regulations foresee compensation for flight delays, cancellation, and overbooking. This is calculated based on the kilometres between the flight origin and destination:

You can also find out by filling out our form. It will take you less than 99 seconds. We will let you know if you are eligible to file a claim and an estimated amount. Free of charge and with no obligation.

Apart from compensation, you have other rights, depending on the case.

Delays:

Cancellation and overbooking:

Whatever your case may be, you can also claim:

Even if you no longer have your boarding pass, you can ask your airline for a boarding certificate. For this, you’ll need to make a written request to your airline. It’s important that you include the following information:

On average, it takes one year. This will depend on many factors, such as if the airline is willing to reach an out-of-court settlement or not.

These are extraordinary circumstances for which a flight may be delayed or cancelled. These are the only cases where it’s not possible to file a claim.

According to European regulations you have up to 5 years to make your claim from the date of the incident, regardless of whether it’s due to a delay, cancellation, or overbooking.

Through the Montreal Convention, you only have 2 years.

Your ID card or passport and your flight tickets or boarding pass are enough to justify and claim your flights.

To speed up the claim process, it’s advised to have one of the following documents at hand:

Generally, if you are in Spain for less than 183 days per year, you are not considered a resident for tax purposes. However, there are exceptions. For instance, if your spouse and children live in Spain, or if the Spanish tax office believes that your core economic interests are in Spain. You can also verify it by answering a few simple questions through our form. In less than 99 seconds.

That’s right. Even if you aren’t renting out your property, you’ll still have to pay what is known as allocated property income. By owning an empty or unused property, other than your ‘primary residence’, and deciding to not rent it out, the Spanish tax authorities consider that you could rent it out and generate income. Therefore they quantify this option for a certain amount and require you to pay tax on it.

If your property has been empty or used by you, a friend, or a relative for free, this would lead to an income allocation and you’ll have to pay tax.

Yes. The Spanish tax office makes no distinction on this matter. You have to pay taxes for allocated income.

If the taxpayer is a citizen of a European Economic Area (EEA) country the rate is 19%. If not, it will be 24%. This rate is applied on the taxable base and will vary depending on whether you are declaring income obtained from renting out the property or for the income allocation.

Yes, each owner must file their own tax return. Even if they are married.

You’ll have to file a tax return for each property you own in Spain.

Yes, you’re required to pay tax for allocated property income. This would amount to the number of days the property was in your name without being rented out, up until the date it was sold. Regardless of any other taxes that you’ll have to submit, such as those related to the sale itself.

If you don’t pay your taxes you would be breaking the law. Even if you live in a different country. It is likely the Spanish Tax Office will begin a verification process and you’ll face surcharges and penalties. These will accumulate until you settle your tax situation.

You’ll need your DNI or NIE handy. If you filed a tax return in Spain last year, we will also ask you for it. If not, we will ask you for the last five digits of your Spanish bank account’s IBAN.

Can’t find your question? You can contact us.

ContactWhat is your legal health status?

Better safe than sorry. The more we know about you, the better we can protect your interests and the more money we can recover for you. You’ll receive a tailor-made diagnosis.

We will tell you everything we know.

24 August 2023

28 December 2022

11 July 2022

24 August 2023

28 December 2022

11 July 2022

What if you get back more money than you expected?

It's normal to not be aware of everything you can claim. The same can be said regarding the protection of your interests. You can find out in under 99 seconds by answering a few simple questions.

I want to startIt's normal to not be aware of everything you can claim. The same can be said regarding the protection of your interests. You can find out in under 99 seconds by answering a few simple questions

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}